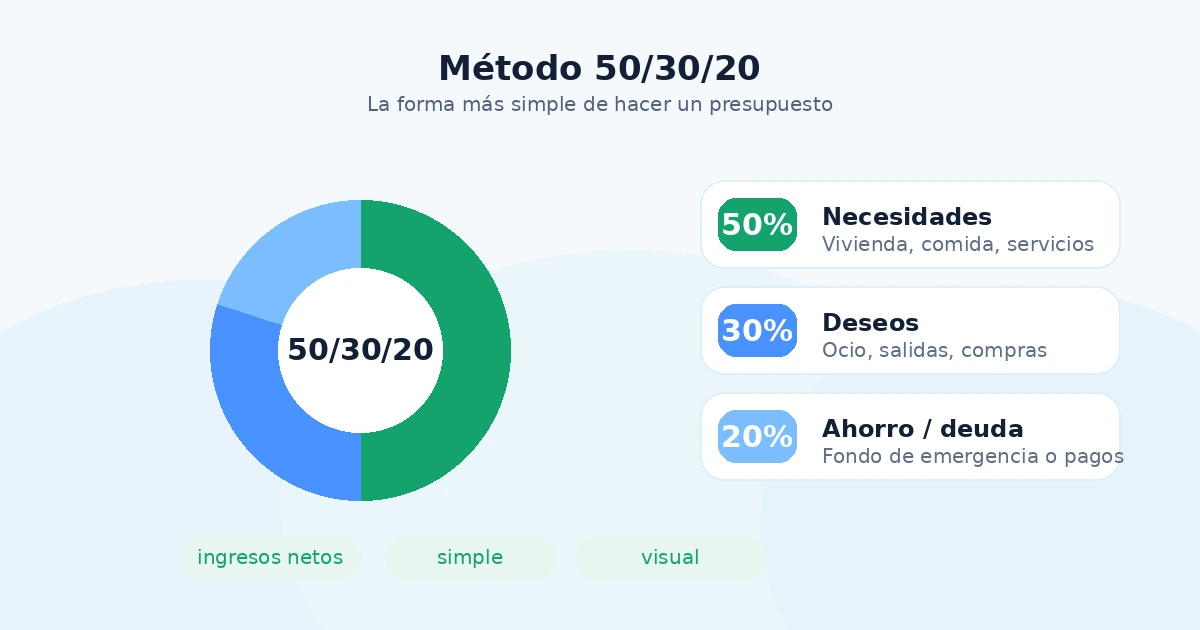

50/30/20 Budget Rule: the simplest way to budget

If you’ve never built a personal budget before, the 50/30/20 rule is probably the best place to start. The premise is simple: split your net income into three buckets — 50% for needs, 30% for wants, 20% for savings and debt payoff — and that’s it. No 40 categories, no complex spreadsheet, no heavy thinking each month.

The simplicity is exactly why it works. The best budget is the one you actually stick to, not the most detailed one. The 50/30/20 rule shrinks the decision friction to almost zero: every expense falls into one of three buckets, and your job is just to keep them balanced.

In this guide we’ll walk through how the method works, what goes in each bucket, examples at different income levels, when it doesn’t fit your situation, and how to track it without drowning in a spreadsheet.

What the 50/30/20 rule is (and where it came from)

The rule was popularized by US senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan (2005). They wanted to offer a simple rule, the opposite of the complex budgets that kept failing in real life.

The reasoning is direct: most people don’t fail their budget for lack of discipline — they fail because of excess complexity. If every expense requires scanning 20 categories, the mental load becomes unsustainable. When every expense falls into one of three buckets, the decision is almost automatic.

The rule isn’t science: it’s a heuristic. And like any heuristic, it works as a starting point, not as an unbreakable law.

How to apply it, step by step

- Calculate your net monthly income. What actually hits your account after taxes and mandatory deductions. Don’t use gross — it would lie to you about the numbers.

- Split that number: 50% to needs, 30% to wants, 20% to savings plus extra debt payments.

- Log every expense and tag it into one of the three buckets for 30 days.

- At the end of the month, compare actual spend against the target percentages.

- Adjust. Almost no one hits the exact ratio in month one — and that’s fine.

What counts as a “need” vs. a “want” (the classic mistake)

This is the source of 80% of issues with the rule.

Need (50%) = something that, if you stopped paying it, your basic life would halt or deteriorate significantly. Rent or mortgage, groceries for home cooking, transit to work, utilities, basic healthcare, minimum debt payments.

Want (30%) = anything else that improves your quality of life but isn’t essential. Dining out and entertainment, food delivery, subscriptions (streaming, gym, apps), non-essential shopping, clothes you buy for fun, vacations, hobbies.

The classic mistake is filing comfortable wants under “needs”. Cable TV is not a need. The unlimited phone plan is not a need (the cheapest plan that works for you is). Food delivery is not a need (food is, but ordered through an app it’s discretionary).

Rule of thumb: if you can cancel it and survive a month without drama, it’s a want.

Debt payments deserve a nuance: the minimum payment lives in “needs” (because skipping it has consequences). Any extra payment to accelerate payoff lives in the 20% bucket.

What goes inside the 20% (it’s not just “money sitting still”)

A lot of people think the 20% is one thing: money parked in a savings account. It isn’t. That 20% splits across 4 destinations depending on where you are financially:

- Emergency fund. First priority if you don’t have one. Initial goal: 1 month of essential expenses. Solid goal: 3 to 6 months. Lives in a separate account you don’t touch.

- Accelerated payoff on expensive debt. If you carry credit-card debt at 25%+ APR, paying more than the minimum is mathematically better than investing. No portfolio gives you 25% guaranteed.

- Savings goals. Trip, move, car, home down payment, grad school. Each goal gets its own sub-bucket, ideally with a clear timeline.

- Investing. Once you have an emergency fund and expensive debt under control, this is where the 20% builds long-term wealth. Index funds, equities, fixed income — but that decision deserves a certified financial advisor.

The ratio between these 4 destinations changes over time. If you’re starting with credit-card debt, the 20% goes almost entirely to debt. As that drops, you redistribute. If you don’t have an emergency fund, that takes priority over investing. It’s not static: it’s an allocation that evolves with your life.

Examples at different income levels

Three realistic cases. Amounts are generic — adapt to your situation and currency.

Example 1 — Low income (~$1,200/month net).

- Needs (50% = $600): shared housing $300, basic groceries $150, utilities $80, transit $70.

- Wants (30% = $360): nights out, streaming, clothes, entertainment.

- Savings/debt (20% = $240).

When income is low, the 50% can feel tight. In practice many people start at 60/25/15 and migrate toward 50/30/20 as income grows.

Example 2 — Middle income (~$3,500/month net, with family).

- Needs (50% = $1,750): rent $900, utilities $180, groceries $420, transit $150, insurance $100.

- Wants (30% = $1,050): family outings, subscriptions, clothes, hobbies.

- Savings/debt (20% = $700): emergency fund, retirement contribution, extra payments.

Example 3 — Irregular income (freelancer). Income swings month to month between $2,000 and $5,000. Strategy: average the last 12 months and budget against the floor. Surpluses from strong months go to the 20% bucket, not to lifestyle inflation. In lean months, the percentages hold but the absolute amounts shrink.

When the 50/30/20 rule does NOT work (the reality for many)

Here’s the part few articles say honestly: for a huge portion of people, the structure of their spending makes the base rule not fit. It’s not a discipline problem — it’s reality. Common cases:

- Your fixed cost of living exceeds 60% of your income. Usually due to expensive housing in any big city (Madrid, Mexico City, Buenos Aires, New York, London). The reality is 65/25/10 and the long-term goal is to bring the fixed cost down or raise income, not torture yourself with the rule.

- You carry severe high-rate debt. If you’re paying 25%+ APR on cards, the 20% is too small. The financial priority is killing that debt, even if it takes 40% of your income for 18 months.

- Your income is just above your minimum cost of living. The 30% for wants doesn’t exist if there’s no slack. First step is raising income.

- Your income is variable or informal. Freelancers, commission sellers, gig workers. Fixed percentages fight with both strong and weak months.

- You have dependents. Kids, aging parents, siblings. The needs bucket inflates for non-negotiable reasons.

- You’re older with no debt and accumulated assets. Optimal distribution shifts when you’re preserving wealth instead of building it.

The conclusion isn’t “abandon the method”. It’s “adjust the percentages to your life”. The 50/30/20 is a starting point, not a straitjacket. What matters is that the savings/investing bucket never hits $0 — even if it’s 5%, keep the habit alive.

That’s why a personal finance assistant that looks at your real numbers — how much comes in, where it goes, which debts weigh the most — is worth more than any rigid rule from a book. It helps you define your percentages based on your reality and adjust them over time.

How to track it without drowning in a spreadsheet

Having the rule is useless without weekly tracking. Three practical options:

- Simple spreadsheet: three columns (needs, wants, savings), log daily, totals computed automatically. Works if you’re consistent.

- Finance app with tags: tag each expense as need/want/savings on top of the regular categories.

- WhatsApp assistant: send the expense by message, voice, or photo; it classifies in real time and tells you what percentage you’re at in each bucket. Zero friction.

The tool matters less than the cadence: check at least once a week whether you’re over, under, or in line with the percentages. Without a weekly review, you only find out about the drift at month end — when you can’t fix it anymore.

What happens next

If you apply the 50/30/20 for 3 months, you’ll discover two things. First, the first month will probably land at 55/35/10 or similar — that’s normal. Second, by month three you’ll have adjusted enough to be close to target, and savings will start to compound.

From month four on you can refine the tool (read how to categorize expenses into 12 universal categories to go beyond the three buckets) or decide whether to stick with the method or switch to something more detailed.

For more context on how this method fits into your overall financial system, see the complete guide to managing personal finances and the practical guide to saving money — where you’ll find a concrete 90-day plan to get started.

Want to apply the 50/30/20 rule without opening a spreadsheet?

Lukrio is a WhatsApp finance assistant that logs your expenses automatically and shows you what percentage you’re at in needs, wants, and savings in real time. Nothing to install.

If this article helped, see also how to categorize expenses, how to run a family budget, and the 7 most common budgeting mistakes.

Frequently asked questions

What is the 50/30/20 budget rule?

It's a budgeting rule that splits your net income into three buckets: 50% for needs, 30% for wants and 20% for savings and debt payoff. It was popularized by Elizabeth Warren and Amelia Warren Tyagi in the book All Your Worth (2005).

Is the 50/30/20 rule based on gross or net income?

Net income: what you actually receive after taxes and deductions. If your income is variable, use the average of the last three to six months as your base and trim the wants bucket during lean months.

What if my fixed expenses exceed 50% of my income?

That's the reality for many people in expensive cities: the split lands at 65/25/10 or similar. Don't abandon the rule; adjust the percentages to your life and keep the savings bucket alive — even at 5% — while you lower fixed costs or raise income.

When does the 50/30/20 rule NOT work?

When you carry severe high-interest debt (killing it comes first), when income barely covers minimum living costs, or when income is highly variable. In those cases fixed percentages fight reality: stabilize first, then apply an adjusted version of the rule.